A serious and long lasting economic downturn in Europe is now within sight. Not a mild recession, but something truly transformative… something similar to the 1930’s great depression. The energy crisis simmering on the back-burner since 2 years now seems to be getting close to its boiling point: with a war in Europe, the blow up and closure of most natural gas pipelines, persistent inflation, drought and a complete global geopolitical rift on top of it all, only luck can save Europe from its fate.

“Labour without energy is a corpse; capital without energy is a sculpture.”

Professor Steve Keen

Energy is the economy. It takes energy to power machines and manufacturing equipment, melt steel, make cement, pour concrete, transport goods and deliver services. It also takes abundant and cheap resources and stable supply chains to run an economy. Take these inputs away and even the strongest economic growth turns into a recession. Our ruling caste’s obsession with ideologies, monetary theories, regulations, policies and digitization, has obscured these simple facts, but the results of their ignorance will be harder and harder to conceal with every passing day. Take the case of Germany, the biggest economy of Europe falling into a recession:

GDP fell by 0.3% for the quarter when adjusted for price and seasonal effects, according to the data from the Federal Statistical Office, Destatis.“After GDP growth entered negative territory at the end of 2022, the German economy has now recorded two consecutive negative quarters,” said Destatis President Ruth Brand. Inflation continued to take its toll on the German economy during the quarter, the office said. This was reflected in household consumption, which was down 1.2% quarter-on-quarter after price and seasonal adjustments. Consumers have seen high inflation erode their purchasing power, reducing demand in the economy. Although the upward price trend has recently eased, the annual inflation rate of 7.2% recorded in April was still relatively high.

German industrial production was especially hurt by a weak performance of the automotive sector, one of the most resource and energy intensive industries relying on a complex web of suppliers. As I wrote nine months ago, the severe energy shortage (made permanent with the eventual destruction of Germany’s Nordstream pipelines) would hit the auto industry especially hard. And while most of these impacts were passed on to consumers in the form of price increases last year, the inflation of essentials (due to the same energetic reasons) has finally turned the tide.

Well, no wonder: if your money buys you less and less food, you finally find yourself postponing the purchase of that new car or that set of new furniture. This is especially true when you consider that food inflation is still much higher than the statistical inflation figures watered down by the services sector:

Food prices now are driving inflation, although the annual increase in food costs was down to 14.9% in May from 22.3% in March. On Tuesday, the statistics office said real wages in Germany were 2.3% lower in the first quarter than a year earlier, despite a 5.6% increase in nominal wages.

Let’s face it: German living standards are falling in tandem with falling energy supplies, despite the government spending billions of Euros to compensate it. Inflation, combined with a sharp rise in interest rates acts as an extra tax on the people: something which they must pay if they want to keep eating and serving their mortgages at the same time (not to mention those, who were forced to take out a loan or live on credit to cover their monthly expenses).

As a result, even large multinational companies see a considerable drop in orders — driven by lower consumer demand. Less orders, of course, mean less purchasing of subcomponents, raw materials and energy. This fall in demand thus starts a causal chain rippling through the entire economy, including suppliers located outside Germany.

A recession in Germany thus means a recession across Europe.

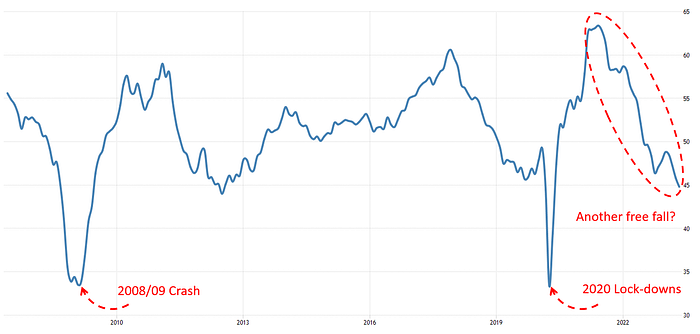

This ripple through effect is well reflected in the metric called Manufacturing PMI, or Manufacturing Purchasing Manager’s Index (1). A number, the fall of which below 50 means that corporate buyers of subcomponents, raw materials and commodities have started to order less as they see a shrinking order book on their side of the business. (For the record: your humble blogger belongs to this purchasing manager group, although, was not surveyed. As someone working in the automotive electrification business, though, I believe what we see here is just the beginning.)

All this decline in demand and orders, combined with a good portion of the German industry leaving the continent earlier this year (due to high energy prices), has resulted in a significant slump in the cost of Natural Gas on the continent, which is now back to 2019 levels. Even better yet, Natural Gas Prices Could Fall Below Zero In Parts Of Europe!

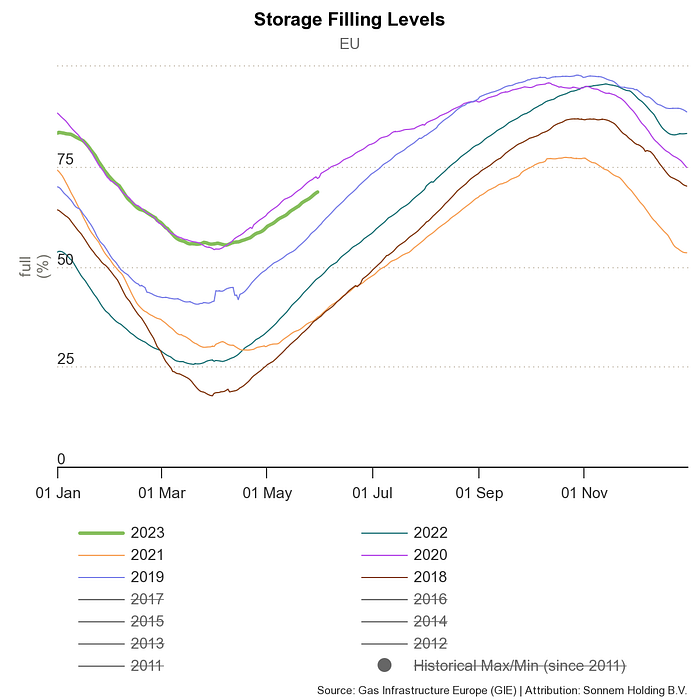

What might seem like a good thing at first glance though, is actually a sign of collapsing demand. Despite the return of low prices, Natural Gas storage is still at a much higher level than usual this time of the year, and not just because of a mild winter. In fact, it is closely tracking the situation in 2020… and we all remember what has happened then (hint: not an economic boom, to say the least). The causes are not particularity hard to decipher here: rising costs of energy (due to scarcity) leads to the inflation of essentials, resulting in a fall of consumer spending. This leads to a similar decline in industrial activity, causing a decrease in energy demand, ultimately leaving most of the gas in storage caverns.

The question presents itself: if we have so much gas, and prices are back to normal again, then why don’t large natural gas consumers remain in Europe? Well, gas prices might be cheap for the moment, but there is also a slackening demand for industrial products (i.e. it’s not worth turning on production for these low order amounts). On the other hand, should consumer spending go up once again, that would eventually drive up natural gas consumption in turn and thus would quickly lead to higher prices. A nice dilemma to say the least.

This brings us back to the lack of consumer demand, largely due to a persistent food inflation. As most of you already know, ammonia based fertilizers are made from natural gas via the Haber-Bosch process. Cheap gas means cheap fertilizers, with their generous use on the fields giving higher crop yields. However, due to the extremely high natural gas prices last year, many producers have simply shut down production. As Irina Slav wrote in oilprice.com article:

Because of fertilizer production shut-ins last year output declined, and prices rose. As a result of this, many farmers probably used less fertilizer than they normally would. And this means lower crops, which would, in turn, mean lower food availability. Add to this plans to essentially eliminate several thousand farms in one of Europe’s biggest agricultural producers, the Netherlands, and the word “crisis” begins to sound a lot more literal than a two-digit inflation rate.

In other words: the seeds of this year’s food inflation were already sown last year, and looking at today’s fertilizer prices we cannot expect a return of cheap food anytime soon; unless there is a permanent slump in industrial natural gas demand. Something got to give: you can choose between a booming economy and low food prices, but in a world of energy and material limits (only made worse by stupid policies) you cannot have both. As to which one will prevail, ask people with an empty stomach.

Now add in the return of drought to Europe placing an additional burden on both agriculture and the energy-industry. According to the latest map of the Combined Drought Indicator 25.9% of the EU-27 territory is in Warning conditions and 8.0% is in Alert conditions… And summer hasn’t started in earnest yet.

With the lack of snow last winter (due to the mild weather), rivers can be expected to be at levels even lower than last year, with reservoirs falling lower still. This not only translates into a reduced water availability for irrigation, but also lower electricity output from hydro dams, reduced industrial water use, higher water temperatures (leading to nuclear power plant shut downs) and lower barge capacities on rivers. If barges cannot be loaded full as it has happened last summer and can carry for example less coal to power plants as a result, this could easily send electricity prices higher still.

This year, the contribution of meltwater to Europe’s water reservoirs “will be really much less than usual,” said Andrea Toreti, a senior researcher at the European Commission’s Joint Research Center. “Because 2023 has been worse than it was last year — and that was already the worst one, looking back at the last 10 years, and now it’s even worse.”

As we have seen, higher energy prices are a drag on the economy and a disaster for consumer goods: not only leaving people with less to spend, but also causing costs to increase in manufacturing. It is hard to see from here, how the real economic output in Europe could avoid falling further still.

One could say, of course that this is all temporary. I hate to be the bearer of bad news, but I see no new sources of cheap energy on the horizon, without which there is little chance for an economic revival. Limits to material and energy extraction are approaching fast, leaving the “hydrogen economy”, nuclear, “renewables” (not to mention “fusion”) to be pies in the sky. Market forces will continue to steer consumption towards essentials (food, clothing) while the discretionary part of the economy slowly withers on the wine.

Deindustrialization in Europe has just begun in earnest — and it is here to stay.

This, of course, is a long slow process not an overnight apocalypse leading to a sudden crash. It will nonetheless lead to increasing unemployment in the industrial sector, further reducing demand for goods and services. The only remaining “hope” for Europe was, at least until recently, to become a cheap assembly plant for Chinese goods (requiring relatively little energy inputs as opposed to manufacturing products from scratch). With recent geopolitical developments though, this too is now definitely off the table. Europe’s ill advised de-risking strategy with its topmost trading partner and the world’s largest manufacturing hub, actually risks shutting off the continent’s last source of cheap goods (including solar panels) and investments.

How the European working class is expected to make a living as deindustrialization rolls on is a question yet to be answered. If the past century is any guide to such matters, though, as economic prospects keep deteriorating so will democracy continue to decline: giving rise to far right ultra-nationalist governments promising to bring back the ‘good old days’, while being ever more hostile to every nation around them. The EU project will be harder and harder to hold together. Minor wars and border disputes are all in the cards, but lacking ample resources, and an industrial base to match, a widespread European war among its nations, however, is off the table for quite a long time.

In its current political environment Europe’s economic ties are unlikely to be reestablished with Russia either. By the time a rapprochement might come (if it ever comes) they too might be starting to experience a decline in oil and gas production — with most of their supplies already sold to other customers across Eurasia. This would leave Europe with a very limited LNG supply from the spot market, as EU politicians were reluctant to make long term contracts with Gulf states due to net zero considerations.

Europe has committed an economic suicide and placed all its bets on a highly volatile, expensive and unreliable LNG market and a renewable boom which is still yet to materialize.

Now, add in the fact that world peak oil production is around the corner (or rather probably behind us), with peak fracked gas and oil supply from the US coming soon, and you start to see where things are headed. Despite all the rhetoric to the contrary, world oil and gas production will start to decline due to reasons rooted in physics and geology, leaving the old continent entirely without suppliers of fossil fuels.

Lacking adequate resources of its own, Europe could soon find itself on the losing side in the battle for fresh water, resources and energy. Global South countries are now openly waving their middle fingers to their former colonizers, and Persian Gulf states (with the last remaining large natural gas fields outside Russia) are brokering long term LNG deals with China instead of Europe.

The geopolitical realignment of the world puts the old continent on a sure path towards becoming a museum for the rest of the world to visit.

Travelers will find an exhibition on “former large capitols of once powerful nations” in the history department, and Petri-dish experiments on “how to live with less-and-less energy and resources on an overheating planet” in the science and technology section. Make no mistake, even though Europe has caused its own untimely demise, this doesn’t mean that the rest of the world could run forever (and a day more) on Earth’s limited resources. Quite to the contrary: Europe’s experience with an energy and resource decline will provide other nations with valuable lessons to learn. Methods to adopt one’s economy to this predicament will be first developed and tested in the old continent and will be spread around the world as the need arises.

Until next time,

B

Notes:

(1) The HCOB Eurozone Manufacturing PMI is compiled by S&P Global from responses to monthly questionnaires sent to survey panels of manufacturers in Germany, France, Italy, Spain, the Netherlands, Austria, Ireland and Greece, totaling around 3,000 private sector companies. The headline figure is the Purchasing Managers’ Index (PMI), which is a weighted average of the following five indices: New Orders (30%), Output (25%), Employment (20%), Suppliers’ Delivery Times (15%) and Stocks of Purchases (10%).