Denial is like a glacier. At first sight, and to everyone standing on it, it looks rock solid. Then cracks start to develop, and before you know it, a huge chunk breaks off and drifts away — never to be seen again. This is what’s happening to peak oil right in front of our eyes: the denial that it cannot possibly come about has started to develop cracks of its own. Yes, peak oil — supposedly “debunked” by the shale revolution — is slowly getting normalized. OK, not in the mainstream media — still chuck full of lunacy and World War III propaganda — but at least in some of the news sites aimed at energy professionals. Some industry journalists have started to slowly realize that it is a very real thing — not a mere theory — and that it won’t be fun to say the least… But let’s just not get ahead ourselves yet.

In my start of the year essay I predicted how peak oil will be announced in 2023 — only to be buried under a pile of BS. Well, here you go, and it’s only March. Paraphrasing Captain Benjamin L. Willard from the movie Apocalypse Now we could say:

“Oh man… the bullshit piled up so fast [in the energy business], you needed wings to stay above it.”

Before we start flapping our wings, first let’s hear the admission that peak oil is not a crackpot theory. As Mr Kern, the Educated Realist from Oilprice.com — “the no.1 source for oil and energy news” — explained with his own words (my emphasis added in bold):

Peak oil is the point in time when worldwide petroleum production reaches its maximum point and begins to decline. It occurs when reserves of easily accessible oil are depleted, and it becomes increasingly difficult and expensive to extract remaining reserves.

One of the primary reasons for peak oil is geological constraints. Most of the world’s easily accessible oil reserves have already been discovered and exploited, meaning that oil companies must turn to more difficult-to-reach reserves, such as deepwater offshore drilling or unconventional sources like shale oil. These reserves are often more expensive to extract and produce smaller yields than traditional wells. As a result, the cost of producing each barrel of oil increases over time.

Geopolitical instability can also play a role in peak oil. Many of the world’s largest oil-producing regions are located in politically unstable areas where conflict and unrest can disrupt production and supply chains. For example, wars in Iraq and Syria have led to significant disruptions in global petroleum production in recent years. And Venezuela’s ongoing economic crisis has absolutely crushed its ability to produce oil.

Technological limitations also contribute to peak oil. Despite advances in drilling technology, there are still limits to how much oil we can extract from a given reserve. Additionally, environmental concerns have made it increasingly difficult to obtain permits for new drilling sites or expand existing ones.

Another factor contributing to peak oil is the rising demand for energy worldwide. As developing countries like China and India continue to grow their economies, their energy needs also increase. This puts additional strain on an already stretched global petroleum industry.

These factors combine to make extracting oil more expensive over time, leading inevitably to a decline in global petroleum production. The consequences of this decline could be catastrophic […]

Wow. Let’s stop here for a minute: according to this article peak oil (supply) not only exists, but it is due to factors outside our influence. Have you noticed? No mention of lack of investment, ESG funds, green policies (except for drilling permits, more on that later), but geology, geopolitics, technical limitations and rising demand, which ultimately cannot be met.

These are the very things I’m (and many others are) blathering about for years now… Man, what’s next? Admitting that there is no infinite growth on a finite planet…?! In case you, dear investor, were scared to death that we will indeed face a long decline, here comes a saving grace from the very same Mr Kern, now the Optimist:

The consequences of this decline could be catastrophic if we do not take action now to transition away from fossil fuels towards renewable energy sources or invest heavily in carbon capture technologies designed to mitigate their impact on the environment.

Oh. My. God. First, how do “carbon capture technologies designed to mitigate their impact on the environment” help us avoiding peak oil supply? Anyway… The real BS comes right after the fold, namely that peak demand might happen sooner and will surely save us:

On the other hand, peak oil demand refers to the point at which global demand for petroleum products begins to decline. This could happen for a variety of reasons, including:

Increased adoption of electric or hydrogen vehicles

Increased availability of consistent renewable energy

Rising oil prices

Environmental concerns

The level of magical thinking on display here gave me an irresistible itch, which could only be scratched by repeating myself: there is no such thing as peak oil demand. Especially not for the reasons stated above. First: rolling out electric vehicles takes a lot of mining and heavy duty transportation — none of which we can electrify. Oil demand would go up as a result of this increased industrial activity (not down), and would drive the prices of the very metals needed to build EV-s sky high, only to crash the renewable/electrified business model consequently. As it reliably did.

Second: renewable electricity is everything but “consistent”, except for its insatiable hunger for metal ores (see the first point above).

Third: a deeply indebted world economy, reeling from an energy shortage for one and a half years now, cannot bear higher oil prices. Instead: demand gets killed, industries close, countries go bankrupt. Oil prices crash as a result, instantly tempering any idea of supply growth.

Fourth: if the environment were that big of a concern as it’s claimed (and by the way as it should be), we wouldn’t open new coal fired power plants all over the planet. But we do, because the economy must keep growing no matter what. And growth means growth in fossil fuel use. Anything else comes in an addition to that, not as a replacement.

Last but not least, dear investor, did you know that copper, lithium, cobalt, even metallurgical grade silicon are finite resources too, just as prone to depletion, price spikes and showing signs of peaking supply as oil itself, which makes them accessible to the industry…? Let that sink in.

I guess it’s time for a more honest admission here. And it comes from no less than Scott Sheffield, the chief executive of Pioneer Natural Resources, the top shale independent in the US:

“The aggressive growth era of US shale is over. The shale model definitely is no longer a swing producer.”

Why is that important? First let’s start by understanding what a swing producer is. In case of any commodity, swing suppliers are the ones who are possessing a large enough spare production capacity, the necessary reserves and an ability to increase or decrease supply at minimal additional internal cost. They are the ones deciding whether supply grows and prices fall, or hold it back to rise prices to customers.

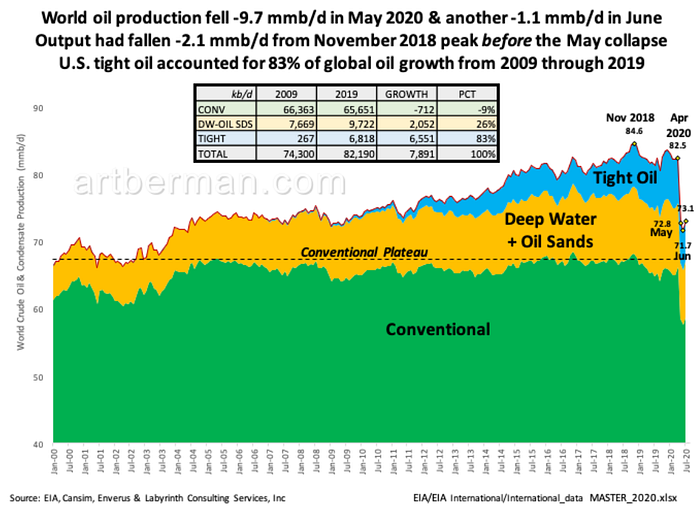

As you can see from the chart above, shale producers played an outsized role in oil ‘production’ growth since conventional sources peaked then plateaued in 2005. Admitting that “the aggressive growth era of US shale is over” and that “the shale model definitely is no longer a swing producer” means that the US can no longer drive oil prices down by increasing production. They must go to the Arab states and plea for more oil (which they don’t have), or tap their strategic reserves if they want to do that. And this is exactly what happened in 2022 — with predictable results.

There are much more to this than what meets the eye at the gas station though. Admitting that the US is no longer a swing producer infers that shale producers no longer have the spare capacity, together with the necessary reserves and the ability to increase or decrease supply at minimal additional internal cost.

In fact it was abundantly clear already back in 2021, that the US Energy Information Administration’s (EIA) shale forecasts were overly optimistic. There are simply a very few sweet spots left to drill. Yes there might be some beneath a national park, or a big city, but it won’t change the fact that oil fields — shale or conventional — are finite things, with a finite area, a finite capacity and a finite amount of oil in them. As for costs, oil companies are facing rapidly increasing costs of equipment, and ever greater scarcity of water and sand used in fracking operations by a thousand truckloads.

Red tape or not, there are limits to growth, and we have hit them.

And not only that. Shale oil is running out fast. Depletion, what was dismissed then ignored a few years ago, all of a sudden gets depicted as completely normal:

Natural depletion is part of life for oil companies. With conventional wells, depletion takes longer to begin and develop. With shale wells, which take much less time to begin producing than conventional wells, depletion also occurs sooner and faster. Shale producers are running out of drilling inventory.

What you read here is a simple admission: existing fracked wells deplete much faster than conventional wells and there are a very few places left to drill for more. Arthur Schopenhauer was proved perfectly right, again:

All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident.

As I wrote about it earlier last year: peak oil is drawing ever closer. And if the calculations are correct peak net energy from oil is expected to arrive in 2023 already. That is this year.

Sit with this, and while at it, ponder how many uses oil has in our high tech lives from mining, to transportation and food production. This means that you cannot expand these activities globally any further, and since peak oil (and peak net energy from oil) means a gradually falling production, this will translate into a permanent crisis. Not a sudden fall or apocalypse. But a steady slimming diet for the economy, turning many parts of it off for good, resulting in less international trade, less travel, less products (including ‘renewables’) and unfortunately less food.

If that’s what you are experiencing — less food at higher prices, companies manufacturing wind turbines going bankrupt in droves due to high metal and energy prices, economic stagnation, bankruptcies — then that’s absolutely no coincidence. The war, sanctions and propaganda all made this worse for sure. Bear in mind though that all these trends were clearly visible already before the tanks started rolling.

Now, there is no way out of this mess other than indeed embarking on a slimming diet. If governments fail to keep up with the loss of oil supply there is more trouble to come however. As Bob McNally, a former adviser to President George W Bush who now runs Rapidan Energy Group told to FT:

“If we end up being more thirsty for oil than the prevailing forecasts assume, then we’ve got big problems. It would be an era of economy-wrecking, geopolitically destabilising, boom and bust swings. That’s when you will wish for more shale.”

This is not an investment advice, but a wake up call: without shale oil there are no real prospects for oil production growth, and with its expected rapid decline, peak world oil supply will soon be a fact of life — not a mere theory. If advisers like Bob McNally worth their salt, world leaders are fully aware of this. Yet the problem was swept under the rug and no realistic transition plan was put in place.

Now, the party is over and the booze is out. Time for a bar fight over who gets to drink the last bottle.

Until next time,

B

PS: if you ever wondered why the West is so eager to contain the biggest economy of East Asia — importing the most oil after Europe, which by the way has just committed itself to an economic slimming diet after banning most of its oil imports — then look no further.