Gutting Germany — Part 3: Diesel

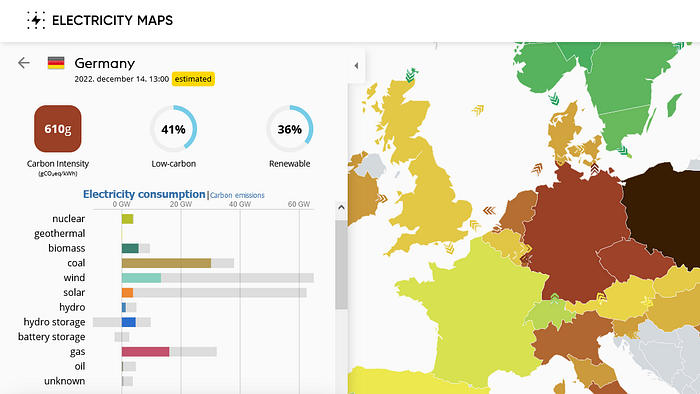

In the past two installments (here & here) we have seen how the geology driven decline in coal production in Germany has led to an increase in natural gas consumption and black coal imports. Now, that Russian coal (50% of German imports) has been sanctioned as of August, and that a range of irresponsible policy decisions (combined with an outright attack on German infrastructure) have led to a 55% loss in gas imports, deindustrialization of Germany seems to be an almost certainty. The killer blow, though, has not arrived yet: the loss of diesel fuel supplies.

Energy is the economy. No energy — no economy. Losing of a half of industrial fuel imports (black coal and gas), will eventually lead to a similar loss of German industrial output over time. As we have seen these fuels can be replaced only in part by very expensive and rather sporadic LNG shipments and an increase in low quality domestic lignite production. This means that while the lights and heat will most probably stay on for most of German residents (at least to those who can afford to pay for them), locally produced goods requiring a lot of energy (like aluminum, glass, steel, fertilizer, paper, chemicals etc.) will have to be replaced with imports — leaving an impoverished nation suffering from high inflation behind. Whether intentionally or not, the initially rejected proposal made by the United States Secretary of the Treasury Henry Morgenthau Jr. in a 1944 seems to be slowly becoming a reality.

The loss of transportation fuel — diesel — elevates the story to a whole new level though. This fuel powers the trucks carrying every single item imported into or produced in a country. From baked bread to microchips there is not a single product which has not took at least part of its journey on a truck. Barges, responsible to carry very large amounts of bulk items from coal to wheat on rivers, also run on diesel — just like ocean faring ships bringing goods from all around the world to Hamburg (and waiting to be refueled there). It is no exaggeration to say, that without an adequate supply of this fuel, transportation of goods first becomes prohibitively expensive, then grinds to a halt.

Another key area where diesel is indispensable is the “production” (in reality: extraction) of finite mineral reserves: lignite burned in German power plants included. Not to mention food… Where 8 kcal of fossil fuels is burned to bring every single kcal to your plate. One can easily see, that even the slightest increase in the price of diesel would be immediately reflected in higher food prices, as well as in increased costs of mineral goods and heavy bulk products like building materials (sand, concrete, chipped stone etc.).

If diesel gets on short supply, higher inflation is all but guaranteed — together with shortages of all kinds.

In 2021 Europe consumed 8% of world gasoline production, yet burned 23% of the world’s diesel — showing how disproportionally reliant the EU is on this particular fuel, and how vibrant its heavy industry and building sector is. (On top of that, diesel is not only burned in heavy vehicles but many cars as well.) Just by looking at these numbers alone, one could come to the conclusion that lowering EU demand could significantly ease the diesel crisis already encircling the globe. As Bloomberg warned recently:

“Within months, almost every region on the planet will face a danger of a diesel shortage just as supply crunches in nearly all the world’s markets have worsened inflation and hurt growth”

The only question remaining is: how to rein in European diesel demand?

Enter the EU embargo on seaborne Russian oil, coming into effect on the 5th of December 2022. Prior to which Germany used to import 31% of its crude oil from Russia... Since it is rather fixed how much diesel you can make out of a single barrel of oil (limitations to chemical composition do apply here) this ban effectively means losing 31% of German diesel supply as well. And that is just fuel lost from raw, crude oil. Germans still have two more months to electrify at least half of their heavy road transport, as Russian refined fuels will be also banned from the European market in February, 2023.

This leaves us with a loss of 500000 barrels of diesel every single day.

Note, that the timing of the oil embargo was combined (conveniently) with the start of the price cap scheme, which prohibits shipping and insurance companies from handling cargoes of Russian crude, unless it is sold for less than the $60 price, set by the G7. At first this measure was communicated to put a cap on Russian revenues, then we were told that it will only put a ceiling on global oil prices. What it will most likely to do, however, is to prevent Russian oil finding its way back to European markets.

What makes me say that? Well, four out of the Group of Seven (G7) countries (Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) pushing this idea happens to be located within Europe. India and China (the other big buyers of Russian oil) were uninterested to say the least, Japan has found its way out of it, while Canada and the US has stopped importing whatever meager amounts of Russian crude they used to buy a long time ago (back on the 28th of February).

This leaves us only with ‘poor, gullible’ European states effectively implementing the price cap (France, Italy, the UK and of course Germany — together with the rest of the EU27). The rest of the world can keep buying Russian oil and diesel at market prices (1). Meanwhile, Russia is on record, repeating in statement after statement, that it will not deliver its oil to any country enforcing this regulation. Russia has lost both the means and the incentive to supply Europe with fuel.

Cutting the cheapest source of supply, on the other hand, will raise diesel prices in Europe, while at the same time, flood the rest of the world (uninterested in this sanctions war) with cheap crude oil and refined fuels. This certainly creates opportunities for price gauging, but most importantly: the embargo on Russian oil and diesel, together with the price cap scheme, will most likely ease the global hunger for diesel and lower the prices at the pump everywhere — except for Europe.

The EU has managed to navigate itself (again) into an immense predicament and has just secured even higher inflation for 2023.

EU refiners, of course, knew that and have loaded themselves chuck full of cheap Russian oil ahead of the ban, while EU fuel storage facilities were also stocking up on (Russian) diesel. The problem is, as always, that these are finite reserves. How long will they last? 1–2 months, if relied on alone? Maybe, combined with a continued delivery from other sources (Saudi, US etc.), they can last 4–6 months...

And then what?

Will OPEC pump more then to help the poor Germans? Hardly. They can’t even fulfill their own reduced quota… How could they extract more? (Besides they are happy with high prices anyway.) Will the US come to the rescue then? Well, apparently they have their own set of predicaments when it comes to oil, as they face the very end to their miraculous shale revolution. Soon they will need more imports themselves.

Amid all this, U.S. oil production growth is slowing down. The shale revolution, as we knew it until a few years ago, is no longer in full-growth mode. And it may never return to it. […] There are numerous reasons for this slowdown, driven, like output growth, by the shale patch. In many parts of the patch, for instance, drillers are running out of so-called sweet spots — low-cost acreage that has driven much of the shale boom.

Good morning! Another well known fact, another thing waiting to happen for a very-very long time now. Every oil field (or shale patch) has a finite area over a geologic formation with clear physical boundaries. Put it bluntly:

If you can count the acres, you can be sure that one day you will run out of them. Together with the oil underneath.

You can put only so many holes in a patch of land before there are literally no places left to drill, let alone liquids to suck out. This is exactly what veteran petroleum geologist J. David Hughes warned us about for over a year now: sweet spots, where oil flows more abundantly are rare and far in between — yet everyone assumed that the entire shale patch is one big sweet spot.

Once you run out of these sweet spots though — which tight oil companies are demonstrably doing right now — your output will first start to flatline then decline no matter how many new wells you drill. And trust me, no one will drill just for the sake of putting nice little holes in the ground: if it doesn’t yield enough oil to justify the investment, then the activity will stop. Factor in price increases for equipment, pipes, diesel (enough to fuel the hauling of one thousand truckloads of sand, water and drilling equipment on site) and we have another nice feedback loop coming into force.

Less wells being drilled of course means falling output. Falling output means rising oil (and consequently) diesel prices. Rising diesel prices increase the cost of drilling, and worsens return on investment — and while choking European diesel supply off slows down the process somewhat, it will do nothing to stop the depletion of oil reserves in America… Rising oil prices can increase supply only up until a certain degree. After a tipping point though drilling wells with ever lower yields (and against exponentially rising costs) will simply not pay for itself.

This is how the oil age ends: it simply won’t worth doing it anymore.

OK, let’s speed up electrification then! As I explained earlier, what all this would do is drive up diesel demand even higher, as mining metals (copper, nickel, lithium etc.) is still done by diesel fueled excavators and dumpers, already eating up 10% of world energy use. And as rich mineral reserves deplete, more and more rocks will need to be hauled uphill from ever deeper pits to satisfy growing demand — something completely left out of the picture (2). With electrification we face an exponential run on diesel — a fuel from which we simply cannot produce enough to cover our current needs, let alone any increases.

Adding a further ironic twist to the story of electrification, but perhaps not surprisingly, Switzerland now considers banning electric vehicle use to avoid blackouts. Yes, you have read it right: its one of the richest countries around the world… Its grid however is highly dependent on imports from Germany (now facing its own issues with the lack of gas) and France (becoming a net importer of electricity after years of neglected maintenance on its nuclear reactor fleet). In this sense Switzerland is the canary in the coal mine: if they have to ban the charging of EV-s, then you can bet that France and Germany will have to follow suit, or make charging vehicles prohibitively expensive for most users.

The circle has become full. As we have seen through the example of Europe in general and Germany in particular, our world is entirely based on fossil fuels. From mining, through manufacturing, transport and electricity generation one cannot get by without burning massive amounts of ancient carbon. This fact not only explains the unsolvable problem of global heating (and the failure of many conferences), but at the same time spells an end to our high-tech civilization.

We live in a finite world, now experiencing hard limits to growth. There is only up to a certain extent we could raise the speed of extraction, and with oil hitting its peak in 2018, it’s quite probable that we have passed a peak in material standards of living as well. A long bumpy ride downhill awaits. At least the worst case climate scenarios have now become nonviable as well.

The self-immolation of the European economy, on the other hand, will only buy humanity just a little time. Nothing more. As oil, gas and coal start their final, long decline the problems created by their loss (inflation, falling standards of living, de-industrialization, ‘renewables’ becoming impossible to finance etc.) will go global and will become even harder to find a way around.

Being complacent and saying that this or that magic technology will replace them (be it Hydrogen, ‘Renewables’, modular reactors, EV-s, etc.) is not only delusional, but suicidal. All these ‘solutions’ require fossil fuels to begin with, not to mention the fact that they are still dependent on drawing down finite resources. Copper. Rare earth metals. Not to mention destroying the only habitable ecosystem we know in the process — the ultimate form of civilizational suicide.

A complex system, like our global civilization, is not thinking ahead however. It adapts only after the fact. It’s leaders will pull whatever levers at their disposal to prolong the fall just a little longer. They will keep trying to overextend their enemies while sacrificing their allies (vassals) in the process — only bringing the very fall they keen to avoid closer and closer. Meanwhile they will keep conditioning their people to believe in magic bullet technologies, evil dictators starting unprovoked wars, and free markets solving every possible issue.

For whom…? For how long…? At what price…?

Don’t ask.

Until next time,

B

Notes:

(1) OK, I forgot about Australia — but how much did they import from Russia anyway?

(2) Surprise, surprise, as a result we’re now facing a looming copper shortage as well! Copper prices are not high enough to justify investment in expanding production, let alone building new mines, all hungry for ever more energy, as rich deposits deplete. Rising copper prices on the other hand would inhibit investment in renewables and electrification in general (ruining the return on investment calculations) — a true catch 22. Profitability in this sector is thus still a pie in the sky — every investor is waiting for extraction to pick up speed so lower prices can return. With rising energy costs, and depleting reserves though, their patience is in wain.